1

Technology: An Economic Definition (技术:经济学定义)

The basic activity of a firm is to use inputs, for example Workers, Machines and Natural resources to produce outputs of goods and services.

📖 点击查看译文

企业的基本活动是利用投入(例如工人、机器和自然资源)来生产商品和服务的产出。

We call the process by which a firm does this a technology; if a firm improves its ability to turn inputs into outputs, we refer to this as a positive technological change.

📖 点击查看译文

我们把企业将投入转化为产出的过程称为“技术”;如果企业提高了这种转化能力,我们称之为“积极的技术变革”。

Technology: The processes a firm uses to turn inputs into outputs of goods and services.

📖 点击查看译文

技术:企业用于将投入转化为商品和服务产出的过程。

Technological change: A change in the ability of a firm to produce a given level of output with a given quantity of inputs.

📖 点击查看译文

技术变革:企业在一定投入条件下生产既定产出能力的变化。

Whenever a firm experiences positive technological change, it is able to produce more output using the same inputs or the same output using fewer inputs.

📖 点击查看译文

每当企业经历积极的技术变革时,就能够在使用相同投入的情况下生产出更多产出,或在保持相同产出的前提下减少投入。

Positive technological change can come from many sources.

📖 点击查看译文

积极的技术变革可能来源于多种途径。

A firm’s managers may rearrange the factory floor or the layout of a retail store in order to increase production and sales.

📖 点击查看译文

企业管理者可能会重新安排工厂车间或零售店的布局,以提升生产和销售。

The firm’s workers may go through a training program.

📖 点击查看译文

企业员工可能会接受培训项目。

The firm may install faster or more reliable machinery or equipment.

📖 点击查看译文

企业可能会安装更快速或更可靠的机器或设备。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Production Process Optimization (生产过程优化)

-

解释 (Explanation):

Optimizing workflows, space, and sequences can increase productivity without changing input quantities.

(通过优化工作流程、空间布置和生产顺序,可以在不增加投入的前提下提高生产效率。)

-

例子 (Example):

Rearranging factory equipment to minimize movement and save time.

(重新布置工厂设备以减少不必要的移动并节省时间。)

-

拓展 (Extension):

Such optimizations are part of operations management and are a low-cost way to achieve technological improvement.

(这种优化属于运营管理范畴,是实现技术进步的一种低成本方式。)

2

The Short Run and the Long Run in Economics (经济学中的短期与长期)

When firms analyze the relationship between their level of production and their costs, they separate the time period involved into the short run and the long run.

📖 点击查看译文

当企业分析其产量与成本之间的关系时,会将所涉及的时间划分为短期与长期。

In the short run, at least one of the firm’s inputs is fixed.

📖 点击查看译文

在短期内,企业至少有一种投入是固定的。

In particular, in the short run, the firm’s technology and the size of its physical plant’s factory, store, or office are both fixed, while the number of workers the firm hires is variable.

📖 点击查看译文

具体来说,在短期内,企业的技术和其工厂、商店或办公室的物理规模是固定的,而雇佣的工人数是可变的。

In the long run, the firm is able to vary all its inputs and can adopt new technology and increase or decrease the size of its physical plant.

📖 点击查看译文

在长期内,企业可以调整所有投入,采用新技术,并扩大或缩小其物理工厂的规模。

The actual length of calendar time before the short run becomes the long run differs from firm to firm.

📖 点击查看译文

从短期过渡到长期所需的实际时间因企业而异。

A pizza parlor may have a short run of just a few weeks before it is able to increase its physical plant by adding another pizza oven and some tables and chairs.

📖 点击查看译文

一家比萨店的短期可能仅为几周,因为它可以在此后通过添加一个比萨烤炉和一些桌椅来扩大其物理设施。

General Motors, in contrast, may have a short run of a year or more before it can increase the capacity of one of its automobile assembly plants by installing new equipment.

📖 点击查看译文

相比之下,通用汽车的短期可能长达一年或更久,因为它需要较长时间才能通过安装新设备来提高其汽车装配厂的产能。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Input Flexibility over Time (投入随时间的可变性)

-

解释 (Explanation):

In economics, input flexibility refers to the firm’s ability to adjust the quantities of resources used in production over different time frames.

(在经济学中,投入的可变性是指企业在不同时间范围内调整其生产资源数量的能力。)

-

例子 (Example):

A small business may quickly hire or lay off workers (variable input), but cannot immediately expand its office space (fixed input).

(一家小企业可能很快就能雇佣或解雇员工(可变投入),但不能立即扩大办公室面积(固定投入)。)

-

拓展 (Extension):

This distinction is crucial in cost analysis and in understanding firm behavior under constraints of time and resource availability.

(这种区分对于成本分析以及理解企业在时间与资源受限条件下的行为至关重要。)

3

The Difference between Fixed Costs and Variable Costs (固定成本与可变成本的区别)

Total cost is the cost of all the inputs a firm uses in production.

📖 点击查看译文

总成本是指企业在生产中使用的所有投入的成本。

In the short run, some inputs are fixed and others are variable.

📖 点击查看译文

在短期内,部分投入是固定的,其他是可变的。

The costs of the fixed inputs are called fixed costs, and the costs of the variable inputs are called variable costs.

📖 点击查看译文

固定投入的成本被称为固定成本,可变投入的成本被称为可变成本。

We can also think of variable costs as the costs that change as output changes.

📖 点击查看译文

我们也可以把可变成本理解为随着产量变化而变化的成本。

Similarly, fixed costs are costs that remain constant as output changes.

📖 点击查看译文

同样地,固定成本是不随产量变化而变化的成本。

A typical firm’s variable costs include its labor costs, raw material costs, and costs of electricity and other utilities.

📖 点击查看译文

典型企业的可变成本包括劳动力成本、原材料成本、电力和其他公用设施的成本。

Total cost = Fixed cost + Variable cost (TC = FC + VC)

📖 点击查看译文

总成本 = 固定成本 + 可变成本(TC = FC + VC)

知识点列表与拓展 (Knowledge Points and Extensions):

1. Cost Classification in the Short Run (短期内的成本分类)

-

解释 (Explanation):

In the short run, costs are divided into fixed and variable components to better understand production expenses.

(在短期内,为了更好地理解生产支出,成本被划分为固定成本和可变成本两部分。)

-

例子 (Example):

A bakery pays monthly rent for its store (fixed cost), and the cost of flour and hourly wages for bakers (variable costs) increases as more bread is produced.

(一家面包店每月支付店铺租金(固定成本),而随着面包产量的增加,面粉和面包师小时工资等可变成本也会上升。)

-

拓展 (Extension):

Understanding the breakdown between fixed and variable costs helps firms make production decisions and evaluate profitability at different output levels.

(理解固定成本和可变成本的构成有助于企业做出生产决策,并在不同产量水平上评估盈利能力。)

4

Costs versus Explicit Costs (隐性成本与显性成本的区别)

Remember that economists always measure cost as opportunity cost, which is the highest-valued alternative that must be given up to engage in an activity.

📖 点击查看译文

请记住,经济学家总是将成本衡量为机会成本,即为从事某项活动而必须放弃的最高价值替代品。

When a firm spends money, it incurs an explicit cost.

📖 点击查看译文

当企业花费金钱时,它就会产生显性成本。

When a firm experiences a nonmonetary opportunity cost, it incurs an implicit cost.

📖 点击查看译文

当企业经历非货币的机会成本时,它就会产生隐性成本。

For example, suppose that Jill Johnson owns a pizza restaurant.

📖 点击查看译文

例如,假设吉尔·约翰逊拥有一家比萨店。

Her explicit costs include the wages she pays her workers and the payments she makes for rent and electricity.

📖 点击查看译文

她的显性成本包括支付给工人的工资以及她为租金和电费支付的费用。

But some of Jill’s most important costs are implicit.

📖 点击查看译文

但吉尔的一些最重要的成本是隐性成本。

Before opening her own restaurant, Jill earned a salary of $30,000 per year managing a restaurant for someone else.

📖 点击查看译文

在开设自己餐厅之前,吉尔每年通过为别人管理餐厅赚取3万美元的薪水。

To open her own business, Jill had to give up the 3,000 in interest.

📖 点击查看译文

为了开设自己的生意,吉尔不得不放弃3万美元的薪水和3000美元的利息。

This $33,000 is an implicit cost because it does not represent payments that Jill has to make.

📖 点击查看译文

这33,000美元是隐性成本,因为它并不代表吉尔必须支付的费用。

Nevertheless, giving up this $33,000 per year is a real cost to Jill.

📖 点击查看译文

然而,每年放弃这33,000美元对吉尔来说是一项真实的成本。

In addition, during the course of the year, the $50,000 worth of tables, chairs, and other physical capital in Jill’s store will lose some of its value partly due to wear and tear and partly due to better furniture, cash registers, and so forth, becoming available.

📖 点击查看译文

此外,在这一年中,吉尔店里价值50,000美元的桌椅及其他实物资本将会贬值,部分原因是因磨损,部分原因是更好的家具、收银机等设备的出现。

Economic depreciation is the difference between what Jill paid for her capital at the beginning of the year and what she would receive if she sold the capital at the end of the year.

📖 点击查看译文

经济折旧是吉尔年初为其资本支付的费用与年末如果卖掉这些资本她能收到的价格之间的差额。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Opportunity Cost (机会成本)

-

解释 (Explanation):

Opportunity cost refers to the value of the next best alternative that must be sacrificed when making a choice.

(机会成本是指在做出选择时必须放弃的下一个最佳替代方案的价值。)

-

例子 (Example):

If Jill decides to open her own restaurant, the opportunity cost includes the salary and interest she gave up, as well as any other alternative uses of her time and resources.

(如果吉尔决定开设自己的餐厅,机会成本包括她放弃的薪水和利息,以及她时间和资源的其他替代用途。)

-

拓展 (Extension):

Economists use opportunity cost to evaluate decisions, helping to understand the trade-offs involved in resource allocation.

(经济学家使用机会成本来评估决策,帮助理解资源配置中涉及的权衡。)

2. Explicit vs. Implicit Costs (显性成本与隐性成本)

-

解释 (Explanation):

Explicit costs are direct, out-of-pocket expenses, while implicit costs represent the opportunity costs of resources owned by the firm.

(显性成本是直接的支出,而隐性成本代表企业拥有的资源的机会成本。)

-

例子 (Example):

Jill’s rent payment is an explicit cost, but the salary she gave up to run the restaurant is an implicit cost.

(吉尔的租金支付是显性成本,但她为了经营餐厅而放弃的薪水是隐性成本。)

-

拓展 (Extension):

Both explicit and implicit costs are important for firms to calculate their true economic costs and profits, and implicit costs can significantly affect a firm’s decision-making.

(显性成本和隐性成本对于企业计算其真实的经济成本和利润都很重要,隐性成本可能会显著影响企业的决策。)

5

Implicit Costs: Additional Examples (隐性成本:更多例子)

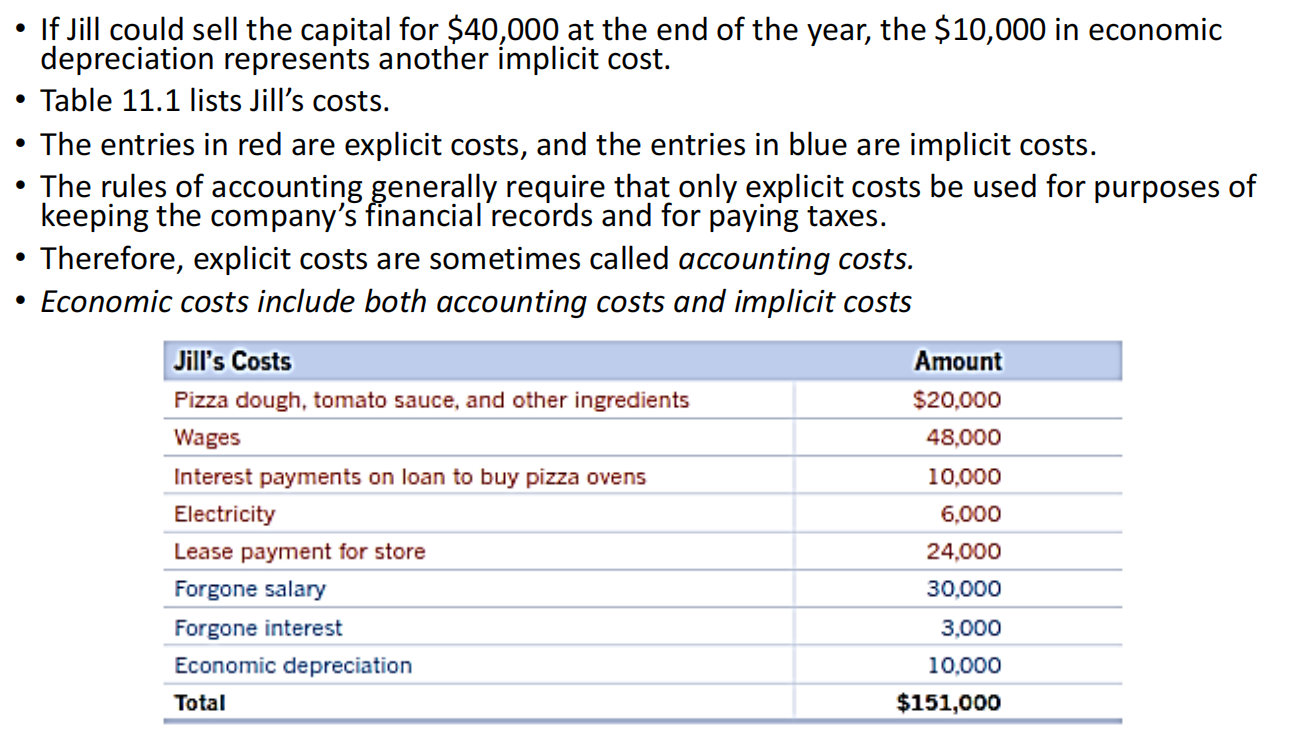

If Jill could sell the capital for 10,000 in economic depreciation represents another implicit cost.

📖 点击查看译文

如果吉尔在年末能够将资本以40,000美元的价格出售,那么10,000美元的经济折旧代表了另一个隐性成本。

Table 11.1 lists Jill’s costs.

📖 点击查看译文

表11.1列出了吉尔的成本。

The entries in red are explicit costs, and the entries in blue are implicit costs.

📖 点击查看译文

红色条目是显性成本,蓝色条目是隐性成本。

The rules of accounting generally require that only explicit costs be used for purposes of keeping the company’s financial records and for paying taxes.

📖 点击查看译文

会计规则通常要求仅使用显性成本来记录公司财务并支付税款。

Therefore, explicit costs are sometimes called accounting costs.

📖 点击查看译文

因此,显性成本有时被称为会计成本。

Economic costs include both accounting costs and implicit costs.

📖 点击查看译文

经济成本包括会计成本和隐性成本。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Economic Depreciation (经济折旧)

-

解释 (Explanation):

Economic depreciation is the loss in value of a firm’s capital over time, often due to wear and tear or technological improvements.

(经济折旧是指企业资本随时间贬值,通常是由于磨损或技术进步所致。)

-

例子 (Example):

Jill’s capital loses value throughout the year, and the $10,000 difference between the initial cost and the sale price represents economic depreciation.

(吉尔的资本在一年中贬值,初始成本与销售价格之间的10,000美元差额代表经济折旧。)

-

拓展 (Extension):

Economic depreciation is an important concept in understanding how businesses assess their true costs and make investment decisions.

(经济折旧是理解企业如何评估其真实成本和做出投资决策的重要概念。)

2. Accounting Costs (会计成本)

-

解释 (Explanation):

Accounting costs are the actual out-of-pocket expenses that a firm incurs, typically considered when recording financial records and paying taxes.

(会计成本是企业实际支出的费用,通常在记录财务记录和缴纳税款时考虑。)

-

例子 (Example):

Jill’s rent, wages for workers, and utility payments are all accounting costs because they involve direct monetary payments.

(吉尔的租金、工人工资和公用事业费用都是会计成本,因为它们涉及直接的货币支付。)

-

拓展 (Extension):

While accounting costs are crucial for financial record-keeping, they do not account for implicit costs such as opportunity costs, which can affect a firm’s overall economic performance.

(虽然会计成本对于财务记录至关重要,但它们并不考虑隐性成本,如机会成本,这些成本可能会影响企业的整体经济表现。)

6

Production Cost (生产成本)

Jill Johnson’s restaurant turns its inputs (pizza ovens, ingredients, labor, electricity, etc.) into pizzas for sale.

📖 点击查看译文

吉尔·约翰逊的餐厅将其投入(如比萨烤箱、食材、劳动力、电力等)转化为待售的比萨。

To make analysis simple, let’s consider only two inputs: The pizza ovens, and Workers.

📖 点击查看译文

为了简化分析,我们只考虑两个投入:比萨烤箱和工人。

The pizza ovens will be a fixed cost; we will assume Jill cannot change (in the short run) the number of ovens she has.

📖 点击查看译文

比萨烤箱将是固定成本;我们假设吉尔不能(在短期内)改变她的烤箱数量。

The workers will be a variable cost; we will assume Jill can easily change the number of workers she hires.

📖 点击查看译文

工人将是可变成本;我们假设吉尔可以轻松改变她雇佣的工人数量。

Jill Johnson’s restaurant has a particular technology by which it transforms workers and pizza ovens into pizzas.

📖 点击查看译文

吉尔·约翰逊的餐厅有一种特定的技术,通过该技术它将工人和比萨烤箱转化为比萨。

With more workers, Jill can produce more pizzas.

📖 点击查看译文

有了更多的工人,吉尔可以生产更多的比萨。

This is the firm’s production function: the relationship between the inputs employed and the maximum output from those inputs.

📖 点击查看译文

这就是企业的生产函数:投入与由这些投入产生的最大产出之间的关系。

The first three columns of Table 11.2 show the relationship between the quantity of workers and ovens Jill uses per week and the quantity of pizzas she can produce.

📖 点击查看译文

表11.2的前三列显示了吉尔每周使用的工人和烤箱数量与她能生产的比萨数量之间的关系。

Because a firm’s technology is the processes it uses to turn inputs into output, the production function represents the firm’s technology.

📖 点击查看译文

因为企业的技术是它用来将投入转化为产出的过程,生产函数代表了企业的技术。

The first three columns of Table 11.2 show Jill’s short-run production function because we are assuming that the time period is too short for Jill to increase or decrease the quantity of ovens she is using.

📖 点击查看译文

表11.2的前三列显示了吉尔的短期生产函数,因为我们假设时间段太短,吉尔无法增加或减少她使用的烤箱数量。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Production Function (生产函数)

-

解释 (Explanation):

The production function describes the relationship between the inputs used in production and the output produced. It reflects the firm’s technology.

(生产函数描述了生产中投入与产出之间的关系,反映了企业的技术。)

-

例子 (Example):

Jill’s production function relates how many pizzas she can produce based on the number of workers and ovens.

(吉尔的生产函数描述了她根据工人和烤箱数量能生产多少比萨。)

-

拓展 (Extension):

The production function can vary depending on the firm’s technology and capacity, and it is crucial in determining how inputs contribute to the final output.

(生产函数可能会根据企业的技术和能力而有所不同,它对于确定投入如何对最终产出产生贡献至关重要。)

2. Fixed Costs (固定成本)

-

解释 (Explanation):

Fixed costs are costs that do not change with the level of output produced.

(固定成本是指不随生产产出水平变化的成本。)

-

例子 (Example):

Jill’s pizza ovens represent fixed costs because the number of ovens does not change in the short run, regardless of how many pizzas are produced.

(吉尔的比萨烤箱代表了固定成本,因为无论生产多少比萨,烤箱的数量在短期内都不会变化。)

-

拓展 (Extension):

Fixed costs are important for determining the firm’s breakeven point and profitability in the short run.

(固定成本对于确定企业的盈亏平衡点和短期内的盈利能力非常重要。)

3. Variable Costs (可变成本)

-

解释 (Explanation):

Variable costs are costs that change as the level of output changes.

(可变成本是指随着生产水平变化而变化的成本。)

-

例子 (Example):

Jill’s labor costs are variable costs because she can adjust the number of workers based on how many pizzas she needs to produce.

(吉尔的劳动力成本是可变成本,因为她可以根据需要生产的比萨数量调整工人的数量。)

-

拓展 (Extension):

Variable costs are key for determining the scalability of a business, as they increase with the level of output.

(可变成本是确定企业可扩展性的关键,因为它们随着产出水平的增加而增加。)

7

8

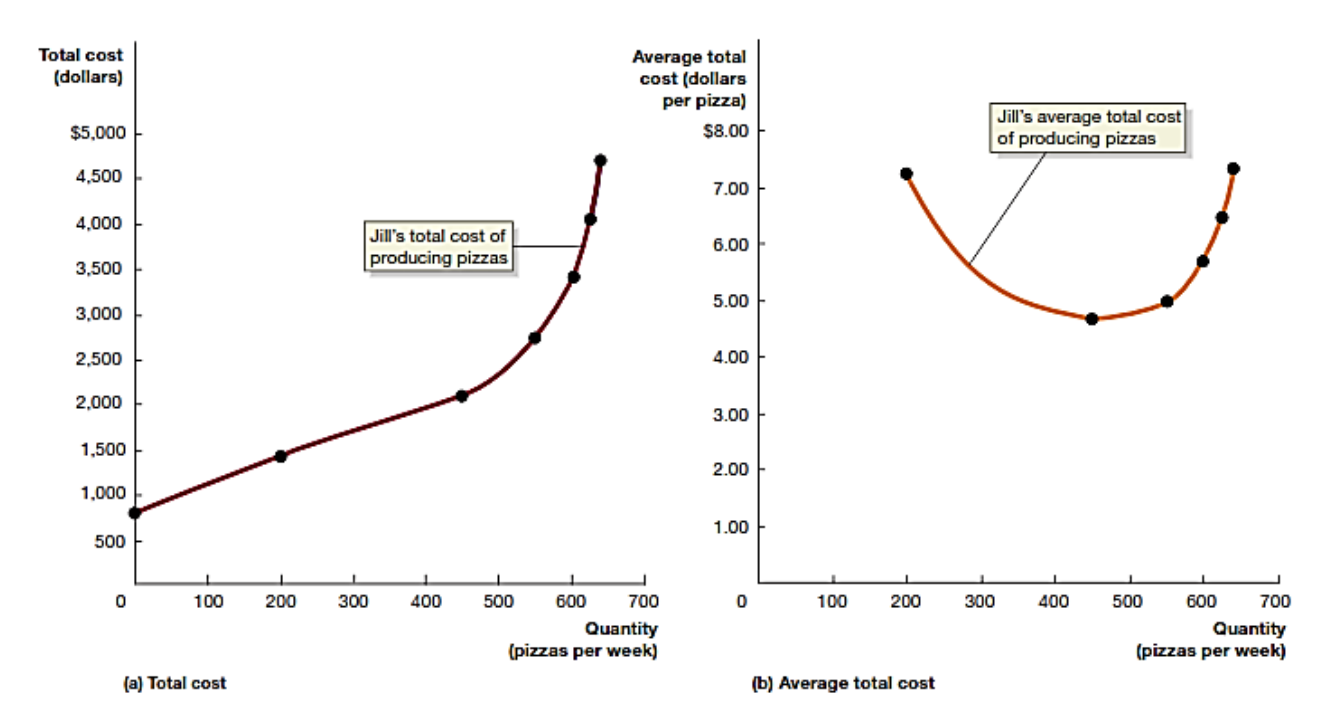

Production Cost Example (生产成本示例)

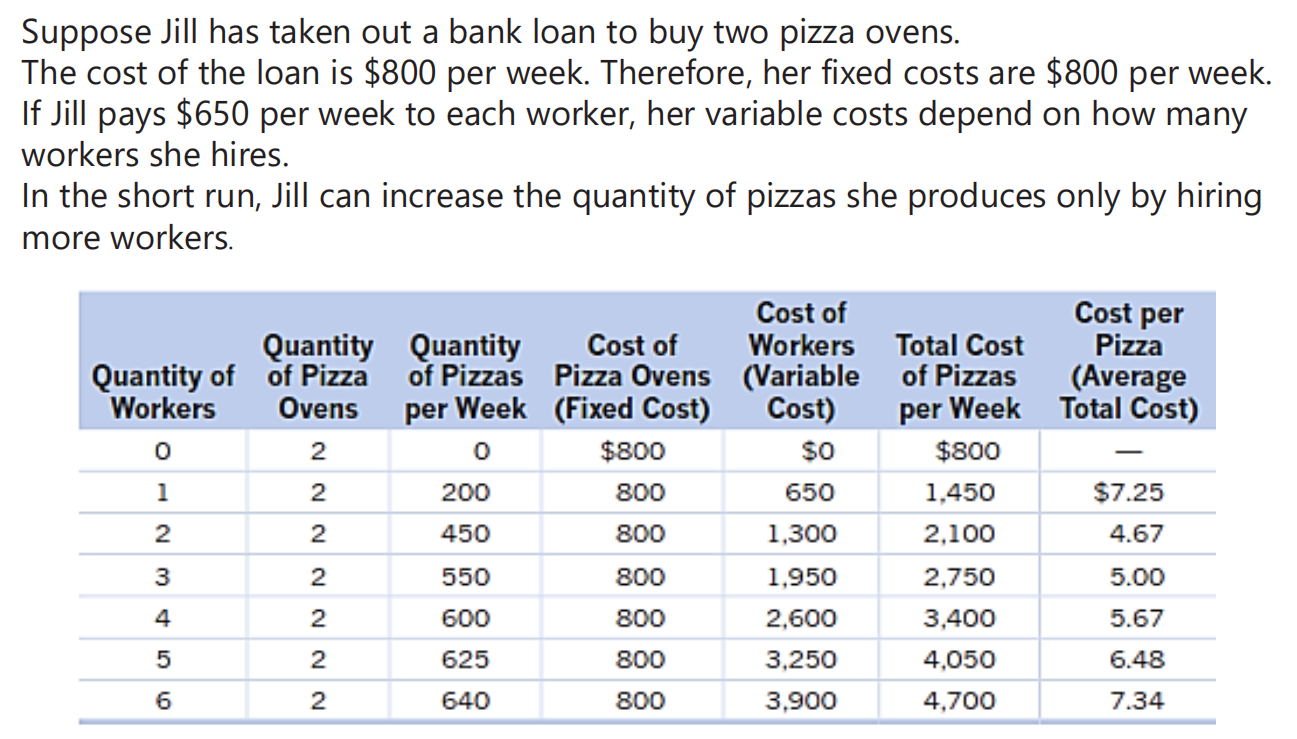

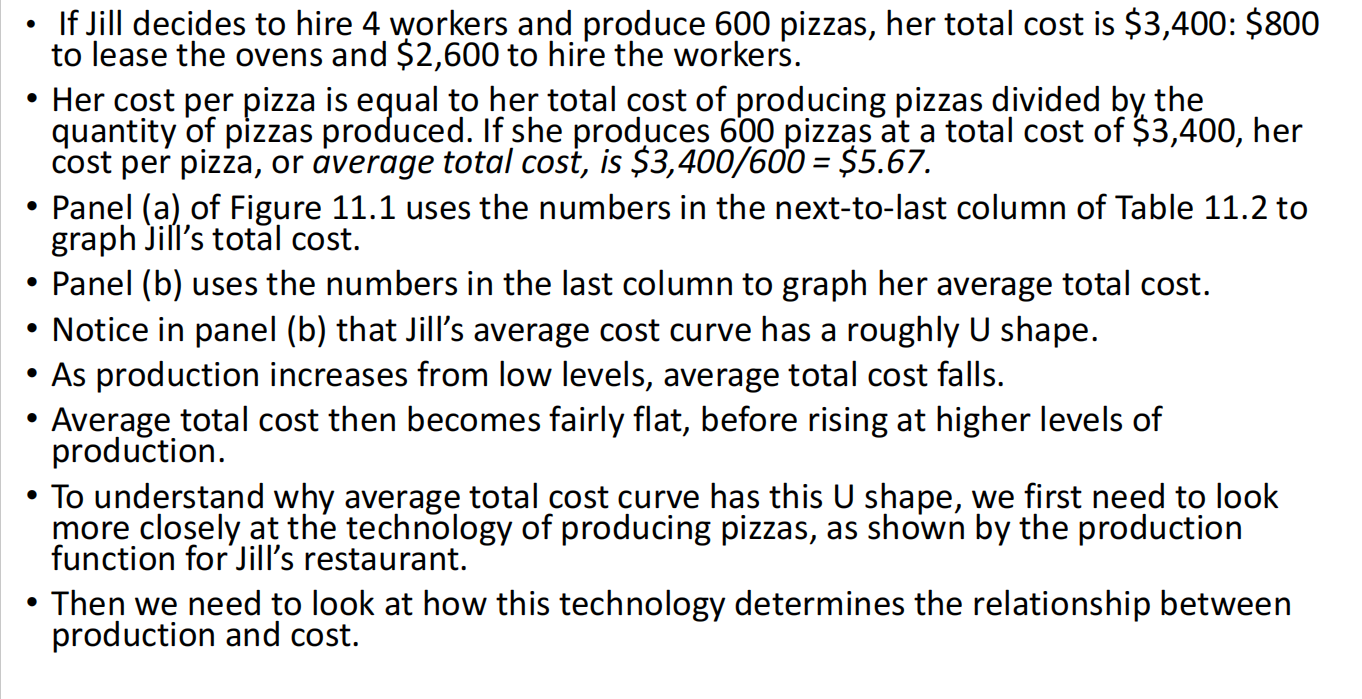

If Jill decides to hire 4 workers and produce 600 pizzas, her total cost is 800 to lease the ovens and $2,600 to hire the workers.

📖 点击查看译文

如果吉尔决定雇佣4名工人并生产600个比萨,她的总成本是3400美元:其中800美元用于租赁烤箱,2600美元用于雇佣工人。

Her cost per pizza is equal to her total cost of producing pizzas divided by the quantity of pizzas produced. If she produces 600 pizzas at a total cost of 3,400/600 = $5.67.

📖 点击查看译文

她每个比萨的成本等于生产比萨的总成本除以生产的比萨数量。如果她以3400美元的总成本生产600个比萨,她每个比萨的成本或平均总成本是3400美元/600 = 5.67美元。

Panel (a) of Figure 11.1 uses the numbers in the next-to-last column of Table 11.2 to graph Jill’s total cost.

📖 点击查看译文

图11.1的面板(a)使用表11.2倒数第二列中的数字来绘制吉尔的总成本。

Panel (b) uses the numbers in the last column to graph her average total cost.

📖 点击查看译文

面板(b)使用最后一列中的数字来绘制她的平均总成本。

Notice in panel (b) that Jill’s average cost curve has a roughly U shape.

📖 点击查看译文

在面板(b)中注意到,吉尔的平均成本曲线呈大致的U形。

As production increases from low levels, average total cost falls.

📖 点击查看译文

随着生产从低水平增加,平均总成本下降。

Average total cost then becomes fairly flat, before rising at higher levels of production.

📖 点击查看译文

然后,平均总成本变得相对平坦,在生产水平较高时上升。

To understand why average total cost curve has this U shape, we first need to look more closely at the technology of producing pizzas, as shown by the production function for Jill’s restaurant.

📖 点击查看译文

为了理解为什么平均总成本曲线呈现U形,我们首先需要更仔细地观察吉尔餐厅生产比萨的技术,如生产函数所示。

Then we need to look at how this technology determines the relationship between production and cost.

📖 点击查看译文

然后,我们需要查看这项技术如何决定生产与成本之间的关系。

知识点列表与拓展 (Knowledge Points and Extensions)

1. Average Total Cost (平均总成本)

-

解释 (Explanation):

Average total cost is calculated by dividing total cost by the quantity of output produced.

(平均总成本是通过将总成本除以生产的产出数量来计算的。)

-

例子 (Example):

Jill’s average total cost is 5.67 per pizza.

(吉尔的平均总成本是3400美元/600个比萨 = 每个比萨5.67美元。)

-

拓展 (Extension):

Average total cost typically decreases at first as production increases (due to economies of scale) and then rises as production becomes less efficient at higher output levels.

(平均总成本通常在生产增加时首先下降(由于规模经济),然后在高产出水平下由于生产效率降低而上升。)

2. U-shaped Cost Curve (U形成本曲线)

-

解释 (Explanation):

The U-shape of the average cost curve is due to economies of scale at first (lower costs with increased production) followed by diseconomies of scale at higher levels of production (higher costs due to inefficiencies).

(平均成本曲线的U形是由于初期的规模经济(随着生产增加成本降低),然后在生产水平较高时由于低效导致的规模不经济(成本上升)。)

-

例子 (Example):

Jill’s cost curve initially falls as she hires more workers and increases production but rises after reaching an optimal level of workers and equipment.

(吉尔的成本曲线在她雇佣更多工人并增加生产时最初下降,但在达到最佳工人和设备水平后上升。)

-

拓展 (Extension):

The U-shape of average total cost curves is a fundamental concept in economics that helps explain firm behavior and cost management in the production process.

(平均总成本曲线的U形是经济学中的一个基本概念,有助于解释企业行为和生产过程中的成本管理。)

3. Total Cost (总成本)

-

解释 (Explanation):

Total cost is the sum of fixed costs and variable costs, which reflects the total expenditure a firm incurs to produce a given level of output.

(总成本是固定成本和可变成本的总和,反映了企业为生产给定水平的产出而支付的总支出。)

-

例子 (Example):

Jill’s total cost of 800 for ovens) and variable costs ($2,600 for workers).

(吉尔的总成本3400美元包括固定成本(800美元用于烤箱)和可变成本(2600美元用于工人)。)

-

拓展 (Extension):

Total cost helps firms calculate pricing strategies, optimize production, and evaluate profitability.

(总成本帮助企业制定定价策略,优化生产,并评估盈利能力。)

9

-

拓展 (Extension):

Understanding the breakdown between fixed and variable costs helps firms make production decisions and evaluate profitability at different output levels.

(理解固定成本和可变成本的构成有助于企业做出生产决策,并在不同产量水平上评估盈利能力。)

4

Costs versus Explicit Costs (隐性成本与显性成本的区别)

Remember that economists always measure cost as opportunity cost, which is the highest-valued alternative that must be given up to engage in an activity.

📖 点击查看译文

请记住,经济学家总是将成本衡量为机会成本,即为从事某项活动而必须放弃的最高价值替代品。

When a firm spends money, it incurs an explicit cost.

📖 点击查看译文

当企业花费金钱时,它就会产生显性成本。

When a firm experiences a nonmonetary opportunity cost, it incurs an implicit cost.

📖 点击查看译文

当企业经历非货币的机会成本时,它就会产生隐性成本。

For example, suppose that Jill Johnson owns a pizza restaurant.

📖 点击查看译文

例如,假设吉尔·约翰逊拥有一家比萨店。

Her explicit costs include the wages she pays her workers and the payments she makes for rent and electricity.

📖 点击查看译文

她的显性成本包括支付给工人的工资以及她为租金和电费支付的费用。

But some of Jill’s most important costs are implicit.

📖 点击查看译文

但吉尔的一些最重要的成本是隐性成本。

Before opening her own restaurant, Jill earned a salary of $30,000 per year managing a restaurant for someone else.

📖 点击查看译文

在开设自己餐厅之前,吉尔每年通过为别人管理餐厅赚取3万美元的薪水。

To open her own business, Jill had to give up the 3,000 in interest.

📖 点击查看译文

为了开设自己的生意,吉尔不得不放弃3万美元的薪水和3000美元的利息。

This $33,000 is an implicit cost because it does not represent payments that Jill has to make.

📖 点击查看译文

这33,000美元是隐性成本,因为它并不代表吉尔必须支付的费用。

Nevertheless, giving up this $33,000 per year is a real cost to Jill.

📖 点击查看译文

然而,每年放弃这33,000美元对吉尔来说是一项真实的成本。

In addition, during the course of the year, the $50,000 worth of tables, chairs, and other physical capital in Jill’s store will lose some of its value partly due to wear and tear and partly due to better furniture, cash registers, and so forth, becoming available.

📖 点击查看译文

此外,在这一年中,吉尔店里价值50,000美元的桌椅及其他实物资本将会贬值,部分原因是因磨损,部分原因是更好的家具、收银机等设备的出现。

Economic depreciation is the difference between what Jill paid for her capital at the beginning of the year and what she would receive if she sold the capital at the end of the year.

📖 点击查看译文

经济折旧是吉尔年初为其资本支付的费用与年末如果卖掉这些资本她能收到的价格之间的差额。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Opportunity Cost (机会成本)

-

解释 (Explanation):

Opportunity cost refers to the value of the next best alternative that must be sacrificed when making a choice.

(机会成本是指在做出选择时必须放弃的下一个最佳替代方案的价值。)

-

例子 (Example):

If Jill decides to open her own restaurant, the opportunity cost includes the salary and interest she gave up, as well as any other alternative uses of her time and resources.

(如果吉尔决定开设自己的餐厅,机会成本包括她放弃的薪水和利息,以及她时间和资源的其他替代用途。)

-

拓展 (Extension):

Economists use opportunity cost to evaluate decisions, helping to understand the trade-offs involved in resource allocation.

(经济学家使用机会成本来评估决策,帮助理解资源配置中涉及的权衡。)

2. Explicit vs. Implicit Costs (显性成本与隐性成本)

-

解释 (Explanation):

Explicit costs are direct, out-of-pocket expenses, while implicit costs represent the opportunity costs of resources owned by the firm.

(显性成本是直接的支出,而隐性成本代表企业拥有的资源的机会成本。)

-

例子 (Example):

Jill’s rent payment is an explicit cost, but the salary she gave up to run the restaurant is an implicit cost.

(吉尔的租金支付是显性成本,但她为了经营餐厅而放弃的薪水是隐性成本。)

-

拓展 (Extension):

Both explicit and implicit costs are important for firms to calculate their true economic costs and profits, and implicit costs can significantly affect a firm’s decision-making.

(显性成本和隐性成本对于企业计算其真实的经济成本和利润都很重要,隐性成本可能会显著影响企业的决策。)

5

Implicit Costs: Additional Examples (隐性成本:更多例子)

If Jill could sell the capital for 10,000 in economic depreciation represents another implicit cost.

📖 点击查看译文

如果吉尔在年末能够将资本以40,000美元的价格出售,那么10,000美元的经济折旧代表了另一个隐性成本。

Table 11.1 lists Jill’s costs.

📖 点击查看译文

表11.1列出了吉尔的成本。

The entries in red are explicit costs, and the entries in blue are implicit costs.

📖 点击查看译文

红色条目是显性成本,蓝色条目是隐性成本。

The rules of accounting generally require that only explicit costs be used for purposes of keeping the company’s financial records and for paying taxes.

📖 点击查看译文

会计规则通常要求仅使用显性成本来记录公司财务并支付税款。

Therefore, explicit costs are sometimes called accounting costs.

📖 点击查看译文

因此,显性成本有时被称为会计成本。

Economic costs include both accounting costs and implicit costs.

📖 点击查看译文

经济成本包括会计成本和隐性成本。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Economic Depreciation (经济折旧)

-

解释 (Explanation):

Economic depreciation is the loss in value of a firm’s capital over time, often due to wear and tear or technological improvements.

(经济折旧是指企业资本随时间贬值,通常是由于磨损或技术进步所致。)

-

例子 (Example):

Jill’s capital loses value throughout the year, and the $10,000 difference between the initial cost and the sale price represents economic depreciation.

(吉尔的资本在一年中贬值,初始成本与销售价格之间的10,000美元差额代表经济折旧。)

-

拓展 (Extension):

Economic depreciation is an important concept in understanding how businesses assess their true costs and make investment decisions.

(经济折旧是理解企业如何评估其真实成本和做出投资决策的重要概念。)

2. Accounting Costs (会计成本)

-

解释 (Explanation):

Accounting costs are the actual out-of-pocket expenses that a firm incurs, typically considered when recording financial records and paying taxes.

(会计成本是企业实际支出的费用,通常在记录财务记录和缴纳税款时考虑。)

-

例子 (Example):

Jill’s rent, wages for workers, and utility payments are all accounting costs because they involve direct monetary payments.

(吉尔的租金、工人工资和公用事业费用都是会计成本,因为它们涉及直接的货币支付。)

-

拓展 (Extension):

While accounting costs are crucial for financial record-keeping, they do not account for implicit costs such as opportunity costs, which can affect a firm’s overall economic performance.

(虽然会计成本对于财务记录至关重要,但它们并不考虑隐性成本,如机会成本,这些成本可能会影响企业的整体经济表现。)

6

Production Cost (生产成本)

Jill Johnson’s restaurant turns its inputs (pizza ovens, ingredients, labor, electricity, etc.) into pizzas for sale.

📖 点击查看译文

吉尔·约翰逊的餐厅将其投入(如比萨烤箱、食材、劳动力、电力等)转化为待售的比萨。

To make analysis simple, let’s consider only two inputs: The pizza ovens, and Workers.

📖 点击查看译文

为了简化分析,我们只考虑两个投入:比萨烤箱和工人。

The pizza ovens will be a fixed cost; we will assume Jill cannot change (in the short run) the number of ovens she has.

📖 点击查看译文

比萨烤箱将是固定成本;我们假设吉尔不能(在短期内)改变她的烤箱数量。

The workers will be a variable cost; we will assume Jill can easily change the number of workers she hires.

📖 点击查看译文

工人将是可变成本;我们假设吉尔可以轻松改变她雇佣的工人数量。

Jill Johnson’s restaurant has a particular technology by which it transforms workers and pizza ovens into pizzas.

📖 点击查看译文

吉尔·约翰逊的餐厅有一种特定的技术,通过该技术它将工人和比萨烤箱转化为比萨。

With more workers, Jill can produce more pizzas.

📖 点击查看译文

有了更多的工人,吉尔可以生产更多的比萨。

This is the firm’s production function: the relationship between the inputs employed and the maximum output from those inputs.

📖 点击查看译文

这就是企业的生产函数:投入与由这些投入产生的最大产出之间的关系。

The first three columns of Table 11.2 show the relationship between the quantity of workers and ovens Jill uses per week and the quantity of pizzas she can produce.

📖 点击查看译文

表11.2的前三列显示了吉尔每周使用的工人和烤箱数量与她能生产的比萨数量之间的关系。

Because a firm’s technology is the processes it uses to turn inputs into output, the production function represents the firm’s technology.

📖 点击查看译文

因为企业的技术是它用来将投入转化为产出的过程,生产函数代表了企业的技术。

The first three columns of Table 11.2 show Jill’s short-run production function because we are assuming that the time period is too short for Jill to increase or decrease the quantity of ovens she is using.

📖 点击查看译文

表11.2的前三列显示了吉尔的短期生产函数,因为我们假设时间段太短,吉尔无法增加或减少她使用的烤箱数量。

知识点列表与拓展 (Knowledge Points and Extensions):

1. Production Function (生产函数)

-

解释 (Explanation):

The production function describes the relationship between the inputs used in production and the output produced. It reflects the firm’s technology.

(生产函数描述了生产中投入与产出之间的关系,反映了企业的技术。)

-

例子 (Example):

Jill’s production function relates how many pizzas she can produce based on the number of workers and ovens.

(吉尔的生产函数描述了她根据工人和烤箱数量能生产多少比萨。)

-

拓展 (Extension):

The production function can vary depending on the firm’s technology and capacity, and it is crucial in determining how inputs contribute to the final output.

(生产函数可能会根据企业的技术和能力而有所不同,它对于确定投入如何对最终产出产生贡献至关重要。)

2. Fixed Costs (固定成本)

-

解释 (Explanation):

Fixed costs are costs that do not change with the level of output produced.

(固定成本是指不随生产产出水平变化的成本。)

-

例子 (Example):

Jill’s pizza ovens represent fixed costs because the number of ovens does not change in the short run, regardless of how many pizzas are produced.

(吉尔的比萨烤箱代表了固定成本,因为无论生产多少比萨,烤箱的数量在短期内都不会变化。)

-

拓展 (Extension):

Fixed costs are important for determining the firm’s breakeven point and profitability in the short run.

(固定成本对于确定企业的盈亏平衡点和短期内的盈利能力非常重要。)

3. Variable Costs (可变成本)

-

解释 (Explanation):

Variable costs are costs that change as the level of output changes.

(可变成本是指随着生产水平变化而变化的成本。)

-

例子 (Example):

Jill’s labor costs are variable costs because she can adjust the number of workers based on how many pizzas she needs to produce.

(吉尔的劳动力成本是可变成本,因为她可以根据需要生产的比萨数量调整工人的数量。)

-

拓展 (Extension):

Variable costs are key for determining the scalability of a business, as they increase with the level of output.

(可变成本是确定企业可扩展性的关键,因为它们随着产出水平的增加而增加。)

7

8

Production Cost Example (生产成本示例)

If Jill decides to hire 4 workers and produce 600 pizzas, her total cost is 800 to lease the ovens and $2,600 to hire the workers.

📖 点击查看译文

如果吉尔决定雇佣4名工人并生产600个比萨,她的总成本是3400美元:其中800美元用于租赁烤箱,2600美元用于雇佣工人。

Her cost per pizza is equal to her total cost of producing pizzas divided by the quantity of pizzas produced. If she produces 600 pizzas at a total cost of 3,400/600 = $5.67.

📖 点击查看译文

她每个比萨的成本等于生产比萨的总成本除以生产的比萨数量。如果她以3400美元的总成本生产600个比萨,她每个比萨的成本或平均总成本是3400美元/600 = 5.67美元。

Panel (a) of Figure 11.1 uses the numbers in the next-to-last column of Table 11.2 to graph Jill’s total cost.

📖 点击查看译文

图11.1的面板(a)使用表11.2倒数第二列中的数字来绘制吉尔的总成本。

Panel (b) uses the numbers in the last column to graph her average total cost.

📖 点击查看译文

面板(b)使用最后一列中的数字来绘制她的平均总成本。

Notice in panel (b) that Jill’s average cost curve has a roughly U shape.

📖 点击查看译文

在面板(b)中注意到,吉尔的平均成本曲线呈大致的U形。

As production increases from low levels, average total cost falls.

📖 点击查看译文

随着生产从低水平增加,平均总成本下降。

Average total cost then becomes fairly flat, before rising at higher levels of production.

📖 点击查看译文

然后,平均总成本变得相对平坦,在生产水平较高时上升。

To understand why average total cost curve has this U shape, we first need to look more closely at the technology of producing pizzas, as shown by the production function for Jill’s restaurant.

📖 点击查看译文

为了理解为什么平均总成本曲线呈现U形,我们首先需要更仔细地观察吉尔餐厅生产比萨的技术,如生产函数所示。

Then we need to look at how this technology determines the relationship between production and cost.

📖 点击查看译文

然后,我们需要查看这项技术如何决定生产与成本之间的关系。

知识点列表与拓展 (Knowledge Points and Extensions)

1. Average Total Cost (平均总成本)

-

解释 (Explanation):

Average total cost is calculated by dividing total cost by the quantity of output produced.

(平均总成本是通过将总成本除以生产的产出数量来计算的。)

-

例子 (Example):

Jill’s average total cost is 5.67 per pizza.

(吉尔的平均总成本是3400美元/600个比萨 = 每个比萨5.67美元。)

-

拓展 (Extension):

Average total cost typically decreases at first as production increases (due to economies of scale) and then rises as production becomes less efficient at higher output levels.

(平均总成本通常在生产增加时首先下降(由于规模经济),然后在高产出水平下由于生产效率降低而上升。)

2. U-shaped Cost Curve (U形成本曲线)

-

解释 (Explanation):

The U-shape of the average cost curve is due to economies of scale at first (lower costs with increased production) followed by diseconomies of scale at higher levels of production (higher costs due to inefficiencies).

(平均成本曲线的U形是由于初期的规模经济(随着生产增加成本降低),然后在生产水平较高时由于低效导致的规模不经济(成本上升)。)

-

例子 (Example):

Jill’s cost curve initially falls as she hires more workers and increases production but rises after reaching an optimal level of workers and equipment.

(吉尔的成本曲线在她雇佣更多工人并增加生产时最初下降,但在达到最佳工人和设备水平后上升。)

-

拓展 (Extension):

The U-shape of average total cost curves is a fundamental concept in economics that helps explain firm behavior and cost management in the production process.

(平均总成本曲线的U形是经济学中的一个基本概念,有助于解释企业行为和生产过程中的成本管理。)

3. Total Cost (总成本)

-

解释 (Explanation):

Total cost is the sum of fixed costs and variable costs, which reflects the total expenditure a firm incurs to produce a given level of output.

(总成本是固定成本和可变成本的总和,反映了企业为生产给定水平的产出而支付的总支出。)

-

例子 (Example):

Jill’s total cost of 800 for ovens) and variable costs ($2,600 for workers).

(吉尔的总成本3400美元包括固定成本(800美元用于烤箱)和可变成本(2600美元用于工人)。)

-

拓展 (Extension):

Total cost helps firms calculate pricing strategies, optimize production, and evaluate profitability.

(总成本帮助企业制定定价策略,优化生产,并评估盈利能力。)

9

评论

0 条正在加载评论...